- >>

- Youth

India's Growth Story: Only Two Sectors Show An Increase In Growth From Last Year

NEW DELHI: On May 31, the Central Statistics Office (CSO), Ministry of Statistics and Programme Implementation, had released the provisional estimates of national income for the financial year 2015-16 and quarterly estimates of Gross Domestic Product (GDP) for the fourth quarter (January-March) of 2015-16.

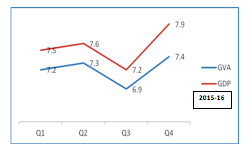

India’s economy grew at 7.9% in January-March 2016, the highest in last six quarters. It is the world’s fastest growing major economy, even out performing China which is growing at a growth of 6.7%. The year on year GDP growth, as estimated by CSO, is 7.6% in 2015-16 from 7.2% in 2014-15. But, if Gross Value Added (GVA) numbers are considered, the annual growth has been just 7.2% in 2015-16 from 7.1% in 2014-15.

GVA is the measure of the value of goods and services produced in an area, industry or sector of an economy. It is the value of output less the value of intermediate consumption.

GVA = Output – Intermediate Consumption (This leads to basic/ input price)

GDP is calculated by summing the Gross Value Added (GVA) of each sector. GVA is at basic price, to which the indirect taxes are added and subsidies are subtracted, to obtain GDP at market prices.

GDP = GVA + taxes on products - subsidies on products (This leads to market price)

In short, GVA is the value added growth excluding taxes and subsidies. This growth had increased marginally from 2014-15 to 2015-16, which is 7.1% to 7.2%. While the increase in annual growth of GDP is higher than GVA, from 7.2% to 7.6%. Major contribution towards GDP growth has come from the drastically reduced subsides by 5.6%.

When analysed, quarter on quarter growth for 2015-16, growth in GVA at basic prices is a more reserved 7.4% for the March quarter, compared to 7.9% GDP. That too is a huge leap on the 6.9% growth in GVA from its previous December quarter. Indeed, the last quarter of 2015-16 has performed great.

What factors led to this good economic performance? Indian GDP is estimated using two approaches; production approach and expenditure approach. GDP estimated by production approach is calculated by evaluation of economic activity of each industry sector.

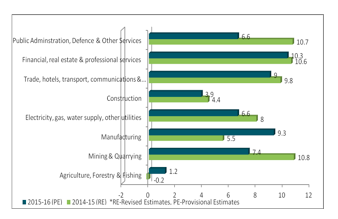

The only two industries which have shown an increase in growth from previous year are Agricultural Sector & Manufacturing Industry.

( '% change over last year')

61% of GVA growth in ‘agriculture, forestry and fishing’ sector is due to fruit and vegetable crops. Around 39% of GVA of this sector is based on livestock products, forestry, fishing and aquaculture.

The other well performing sector, manufacturing has seen an expansion in GVA, mostly due to higher margins being reported by manufacturing firms due to the fall in input prices.

GVA estimated by Expenditure approach, is calculated by evaluating income available in the form of final consumption or saving or capital formation.

( '% change over last year')

If the expenditure pattern of the GDP is noted, private consumption increased by 7.4% in 2015-16 compared with 6.2% increase seen in 2014-15, gross fixed capital formation declined by 3.9% in 2015-16 compared with 4.9% increase seen in 2014-15 indicating that the investment cycle remains more or less stalled.

Government expenses on various administrative services like defense, law and order, education etc. have decreased. Exports have fallen, adding to the woes of stagnation. Reduction in inventories again is a sign of less demand and consumption.

However, reduction in imports is a breather to stabilise the falling exports. Expenditure on valuables have reduced, which is a positive aspect. This means money on valuables like Gold, Gems have reduced, leading to more unlocked money in the market for better consumption or capital formation.

With the predicted normal or good monsoon due to La Nina effect in 2015-16, a continued better agricultural produce is expected. Overall, on the production side, GVA growth is expected to accelerate in financial year 2017.

On the expenditure front, consumption demand is expected to stay buoyant with better rural incomes from good agricultural produce. Urban consumption is also expected to remain on the higher side with the 7th Pay Commission awards and also due to stable inflation and interest rates.

However, the private sector investment cycle is not expected to reverse sharply as capacity formation levels remain low. The other drag on the economy could be from the external sector where the exports are not expected to show any significant uptrend soon. Government expenditures and a target towards boosting investments in power, roads and railways will set the basis for future growth.